GUIDES & SERVIES

Company Registration

How to Register a Company in Poland: A Complete Guide for Foreign Investors

Company formation in Poland

Poland has become a popular place for entrepreneurs who want to launch a new business entity in a stable and well-regulated EU market. Investors appreciate the country’s straightforward corporate rules, accessible registration procedures and the flexibility to choose a structure that suits their plans, whether for a small venture or a larger operation.

Before taking the first formal step, it is useful to gain a clear picture of how the Polish system works and what decisions need to be made early on. This introduction offers a simple, practical starting point so you can approach the company incorporation process with confidence and clarity.

What Makes Poland an Attractive Place to Start a Business?

Many foreign entrepreneurs choose Poland due to a combination of:

- Attractive tax incentives, including reduced corporate tax rates, the Estonian CIT model for reinvested profits, and preferential schemes such as IP Box and R&D relief.

- Strong macroeconomic fundamentals as one of the largest and steadily growing economies in the European Union, supported by a market of over 38 million consumers and a workforce of approximately 15 million people.

- Access to a well-educated talent pool, with around 450 universities and more than one million students contributing to a competitive labour market.

- A strategic geographic position, offering efficient connectivity through major motorways, airports and one of the largest rail networks in the EU, enabling companies to serve both Western and Eastern Europe from a single base.

Which Legal Forms Should You Consider When Setting Up a Company in Poland?

Choosing the right legal structure is an important early step when planning to operate in Poland, as each form differs in terms of liability, governance and regulatory requirements. Foreign investors most often choose a limited liability company, mainly because it offers separate legal personality and shields shareholders from personal exposure, but Poland provides a broad range of additional options.

Below is an overview of the structures available under Polish law, which you may explore to determine which format best suits your project’s objectives and risk profile.

Corporate companies (separate legal personality)

These forms are typically preferred when investors want clear liability separation between the company and its owners.

- Limited Liability Company (Sp. z o.o.)

- Joint Stock Company (S.A.)

- Simple Joint Stock Company (P.S.A.)

Partnerships

Partnership structures generally involve more direct partner responsibility and do not always provide the liability limitation characteristic of corporate entities.

- Civil Law Partnership (S.C.)

- Registered Partnership (Sp.j.)

- Professional Partnership (Sp.p.)

- Limited Liability Partnership (Sp.k.)

- Limited Joint Stock Partnership (S.K.A.)

Other forms of conducting business

Some foreign companies consider alternative structures when they do not require a full corporate vehicle.

- Representative office

- Branch of a foreign company

What Documents Do You Need to Establish a Company in Poland?

The documentation required for setting up a company in Poland depends on who will become the shareholder. When the investor is an individual, the process is straightforward – an ID or passport is usually sufficient, provided it can be presented either in person or through a recognised electronic signing method.

If the shareholder is a foreign legal entity, the requirements are more formalised. The company must provide an excerpt from its home country’s commercial register, issued with Apostille or legalisation when necessary. In addition, identification documents of the persons authorised to act on behalf of that foreign company are needed to complete the application.

For investors forming a company remotely, Polish law allows the entire process to be handled online. In such cases, shareholders may issue a notarial power of attorney, enabling lawyers to sign the incorporation documents and submit all filings on their behalf. The power of attorney must also be Apostilled or legalised before it can be used in Poland.

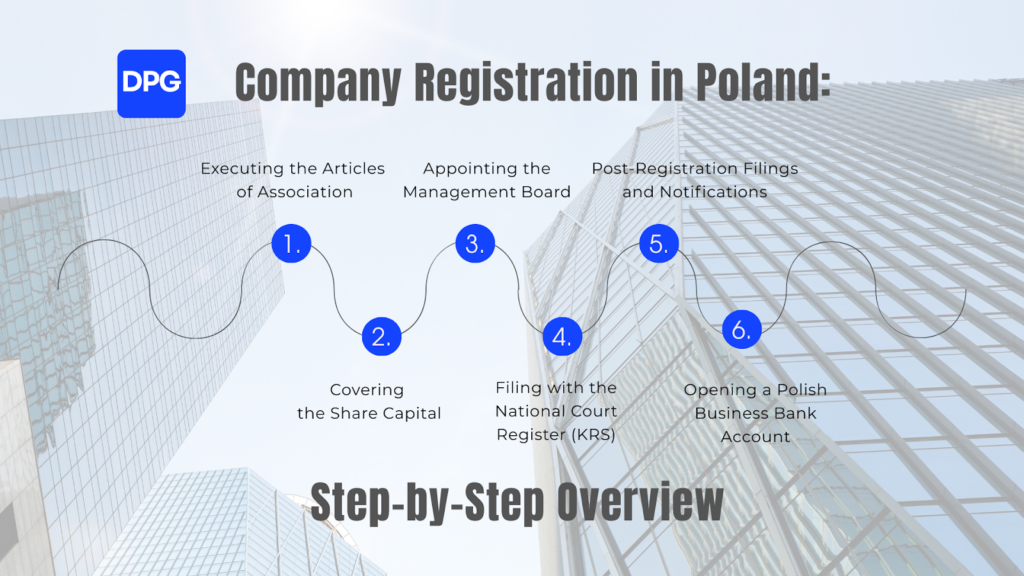

How Does the Company Registration Procedure Work in Poland?

Registering a company in Poland follows a clear six-step sequence set out in the Commercial Companies Code. Each stage plays a specific role in bringing the new entity into legal existence and preparing it for full operation. While the process is similar as in other countries, e.g.: UK: Company House; US – Delaware State: Division of Corporation, Poland applies its own procedural rules and digital tools to complete corporate formation efficiently.

1. Signing the Company’s Articles

The formation process begins when shareholders sign the articles of association, either before a notary or through the designated online portal using an electronic signature. This document defines the company’s core structure, and shareholders may act personally or through authorised attorneys when signing.

2. Providing Contributions to Share Capital

In the traditional notarial route, shareholders must provide contributions toward the share capital immediately after the articles are executed. Online incorporation, however, allows this step to be completed at the end of the process, letting investors pay the initial capital after the company has already been entered into the court register.

3. Appointing the Management Board

Once the company agreement is signed and capital arrangements are clear, shareholders appoint the Management Board, which may consist of one or several members. They act as the company’s representatives and authorised signatories, with their rights defined in the articles or in shareholders’ decisions.

4. Filing the Application with the national court register

The next step is submitting the incorporation application to the National Court Register through either the PRS system (for notarial mode) or the S24 platform (for online filings). Entries made via S24 are usually processed faster, sometimes within 48 hours, while applications in PRS may require several weeks depending on court workload.

5. Completing post registration compliance

After the company is entered into the register, several mandatory follow-up filings must be completed. These include reporting the ultimate beneficial owner, settling the civil law transactions tax (PCC-3), and submitting NIP-8 and, where appropriate, VAT-R forms. Additional permits or sector-specific authorisations may be required depending on the planned activity.

6. Opening the Business Bank Account

To operate effectively, the new foreign entity needs a Polish bank account. While the law does not always require a local account, in practice it becomes essential because only Polish accounts support certain tax and social security payment modules and appear on the tax administration’s whitelist for deductible transactions.

Online and Remote Company Registration Options in Poland

Full Remote Incorporation for Individual and Corporate Shareholders

Polish regulations allow investors to complete the entire incorporation process without travelling to Poland, which is particularly convenient for international projects. Thanks to dedicated online systems and secure electronic signatures, both individual and corporate shareholders can establish a company remotely from their home jurisdiction.

Role of Legal Representatives in Remote Procedures

Where investors prefer not to handle filings personally, lawyers may carry out the process under a notarial power of attorney. This authorises them to sign incorporation documents, prepare digital submissions and communicate with the court on the shareholder’s behalf. The power of attorney must be properly Apostilled or legalised before use in Poland.

Timeline for Online Registration

The remote process is typically efficient, with registration through the online platform often completed within one to three business days. This makes remote incorporation an attractive option for companies seeking quick entry into the Polish market.

Financial and Tax Benefits for New Companies in Poland

| Incentive | Description |

| Reduced Corporate Income Tax Rates | A discounted 9% CIT applies to smaller companies with annual revenue not exceeding EUR 2 million. Larger entities apply the standard 19% CIT. Both thresholds are clearly defined and commonly used by foreign investors. |

| 0% Taxation Under the Estonian CIT System | Companies that reinvest profits rather than distribute dividends may benefit from 0% tax on retained earnings, provided they meet specific conditions (e.g., minimum three full-time employees, only natural persons as shareholders, predominantly operational income). Certain sectors, including financial institutions and SEZ operators, are excluded. |

| Preferential IP Box Regime | Income derived from qualifying intellectual property may be taxed at a 5% rate, provided the company maintains proper IP tracking and documentation linking revenues to protected IP assets. |

| Enhanced R&D Relief | Companies carrying out research or development activities may deduct up to 200% of eligible expenses from their tax base, significantly reducing the effective tax burden. |

| Benefits in Special Economic Zones (SEZ) | Businesses located in SEZs may negotiate corporate income tax or property tax exemptions, depending on project scale, location and investment profile. Terms are granted individually by the zone’s managing authority. |

Post-Registration Obligations for Newly Formed Companies in Poland

Electronic Signatures for Management Board Members

Every director must hold an e-signature compliant with Polish requirements or an ePUAP trusted profile. This signature is essential for routine corporate duties, most notably for signing and submitting annual financial statements to the National Court Register.

Reporting the Ultimate Beneficial Owner

Newly incorporated companies must report their ultimate beneficial owner to the Central Register of Beneficial Owners (CRBR). The filing must be completed within seven days of registration and kept up to date whenever ownership or control structures change.

Civil Law Transactions Tax (PCC) Filing and Payment

Executing the company agreement triggers a duty to file PCC-3 and pay civil law transactions tax at a rate of 0.5% of the share capital. This must be settled within 14 days from the date the articles of association were signed.

VAT Registration Where Required

While not every company must register for VAT immediately, most operational businesses will need VAT status to conduct day-to-day transactions. The VAT-R filing is submitted to the tax office and typically requires confirmation of the company’s registered address.

Obligations Toward the Social Insurance Institution

If a single individual holds all, or nearly all, shares in the company, that person may be required to register with the Social Insurance Institution (ZUS). This obligation depends on the company’s ownership structure and applies in specific situations outlined in Polish regulations.

Fiduciary Company Formation as a Fast-Track Incorporation Method

How Fiduciary Incorporation Works

Some investors choose a fiduciary model when they need a new Polish company to be established quickly. Under this arrangement, the law firm first incorporates the entity under its own name and then holds the shares in trust until they are transferred to the client. From the outset, directors designated by the client are appointed, giving the client full control over the company’s operations while the formalities are finalised.

Advantages of the Fiduciary Model

This structure provides a faster setup compared with standard procedures, as the foundational steps are completed immediately upon the client’s instruction. It reduces administrative delays, limits bureaucratic involvement and enables investors to begin organising their Polish activities sooner, while maintaining full compliance with legal and professional standards.

How It Differs from a Shelf Company

A fiduciary incorporation should not be confused with a shelf company. A shelf company is an already existing entity waiting for purchase, whereas the fiduciary model involves creating a brand-new company tailored to the client’s requirements. The fiduciary company is incorporated only once the client provides instructions and includes the exact structure, name and capital selected for the project.

Summary

Setting up a company in Poland is a structured and accessible process supported by clear statutory rules and modern registration tools. Investors may choose from several legal forms, prepare documentation suited to their profile and complete incorporation through either a notarial or online route.

Once registered, the company must meet a number of compliance obligations, including reporting, tax notifications and operational formalities. Poland’s tax incentives, economic stability and strategic location make it an appealing environment for international entrepreneurs seeking to establish or expand their presence in the region.

FAQ: Company incorporation in Poland

What identification numbers will a Polish company receive during the registration process?

A newly incorporated entity obtains a tax identification number, REGON and KRS entry once the court approves the filing, and these identifiers form the basis for its operation within the polish company register.

What is the minimum share capital required for a limited liability company LLC established by foreign investors?

The minimum share capital for a limited liability company LLC is PLN 5,000, and the founders may deposit share capital either before registration or, in the online procedure, shortly after the company is entered into the register.

Can a foreign entity hold full foreign ownership in a Polish company?

Yes. Polish corporate law permits foreign ownership, whether the shareholder is an individual or a parent company, and the entity will function as a separate legal entity distinct from its participants.

Which authorities oversee tax obligations once the company begins business in Poland?

After incorporation, the company must submit tax forms, including VAT-R and NIP-8, to the competent tax office, which supervises ongoing compliance and records the company’s company address for official correspondence.

Are there filing fees or registration tax applicable during the company incorporation process?

Yes. The court charges filing fees for reviewing the application, and signing the company agreement triggers registration tax, which is calculated on the value of the share capital and treated as a form of transfer tax.

Can the entire registration process be completed remotely through company online systems?

Yes. Foreign investors may complete the entire registration process using company online platforms, and may appoint lawyers to act on their behalf when they require professional assistance or legal services during the company incorporation process.